Artificial intelligence in accounting is the need of the hour. Here are four reasons you should upskill.

Artificial intelligence (AI) is supercharging everything in accounting—from detecting record-keeping errors to making predictions about future expenses. Clients want to use it, and accounting firms want to provide it to clients. But they both need people who can understand the technology and help implement it.

AI application in accounting has been underway for some time now, but the pandemic accelerated its pace. Accounting professionals had to pivot and adapt to new ways of doing things, such as auditing clients remotely and sharing data online. But one of the biggest challenges is the scarcity of skilled accountants who can work alongside these intelligence systems.

A survey shows that 57% of chief finance officers (CFOs) look for AI and machine learning (ML) skills in new hires. If you’re an accountant looking to future-proof your career, gaining AI skills is a great way to differentiate yourself from peers.

In this article, we discuss four reasons accountants like you should adapt their accounting skills for AI and why it’s the right time to diversify your talents.

What is the role of AI in accounting?

In accounting, artificial intelligence is used for various purposes such as detecting fraudulent transactions, automating routine tasks (e.g., maintaining records, processing invoices), and making informed decisions in line with the company's financial health. Small and midsize businesses (SMBs) also invest in AI to reduce labor costs.

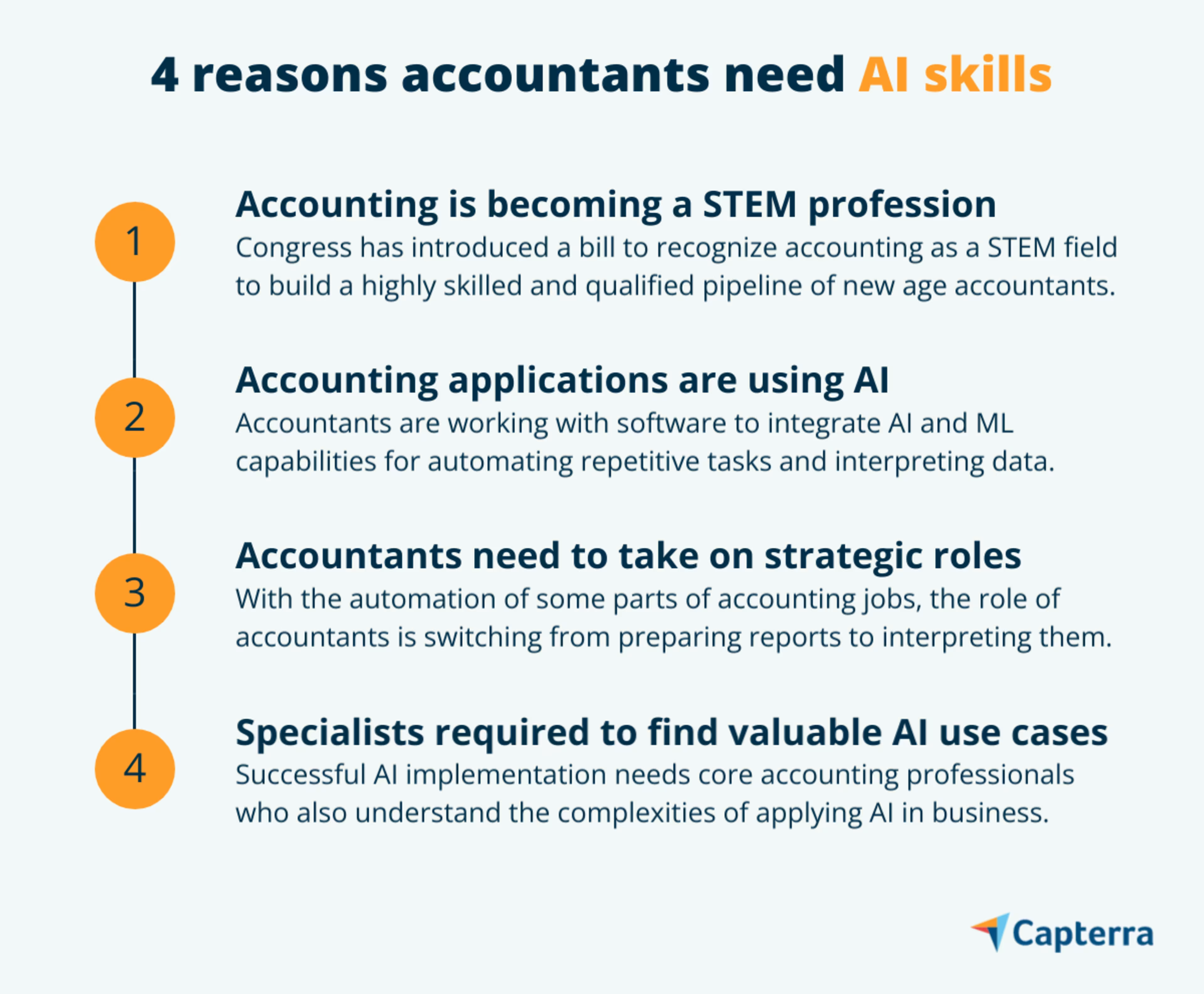

Reason #1. Accounting is becoming a STEM profession

The idea that accounting is a technological profession is gaining ground. Multiple interest groups are working to get accounting recognized as a science, technology, engineering, and mathematics (STEM) career.

In June 2021, Congress introduced the Accounting STEM Pursuit Act of 2021 with the support of both parties. About this development, the American Institute of Certified Public Accountants (AICPA), Center for Audit Quality, and National Association of Black Accountants said, “STEM recognition for accounting will help to diversify and build a highly skilled and qualified pipeline of accountants in the United States.”

What does this mean for you? The high-tech nature of accounting becomes official with this law. Accountants of the future will use robots to actively manage and analyze the large volumes of data (or big data) generated by their business functions and work along with IT professionals to further digitalize and automate their departments.

Expand your subject expertise to emerging technologies. Be an early adopter of tech skills, and lead technology adoption for your accounting firm or department by asking yourself:

How can you integrate various accounting processes and technology?

How can you innovate the current accounting workflow?

Check the last section for a list of skills you should begin with.

Further reading: 9 Basic (and New) Accounting Skills You Need for Success

Reason #2. Accounting applications are increasingly using AI

Accounting solutions are evolving to offer features beyond transactional processes such as data entry. Tools integrated with AI and ML capabilities are being used to automate repetitive tasks such as processing invoices, capturing data from PDFs, and making payments.

By 2025, technologies enabling hyper automation will deliver more than 50% of work for finance and accounting BPO firms, according to Gartner. Hyper automation is an approach to digitalization that uses technologies such as ML and AI to automate complex tasks that need human judgment, such as the analysis of financial statements.

What does this mean for you? Technology advances will continue to push accountants’ power to interpret data. Previously, they shifted from pen and paper to calculators to spreadsheets to data entry tools. Now, they need to ace technologies such as AI and ML to detect patterns and outliers in financial data and help business leaders make the right decision.

Find out where your interests lie in this marriage of accounting and technology.

With a grip on AI and data analytics, you can become an in-house accountant who uses automation to improve day-to-day processes, a finance expert providing specialized services in visualizing data or predicting future outcomes (see prescriptive analytics), or a consultant with an overarching expertise in digitalizing the finance and accounting industry.

As you learn more about implementing AI, refer to these commonly used ML and AI capabilities in accounting solutions:

Spectrum of AI in accounting: A quick overview

Intelligence optical character recognition (OCR) | OCR technology uses computer vision to understand data in scanned images. Accounting applications combine multiple OCR engines to digitize documents and use AI to best capture a document or an image, extract data from it, and correct common errors that would normally be done by a human—and they do all of this with high accuracy. |

Machine-readable invoices | ML is used to peruse documents in readable text format and extract data with much higher accuracy rates than the OCR technology used for images. |

Fraudulent invoice detection | AI engines can look for duplicate or fraudulent invoices by perusing the entire contents of an invoice instead of just checking the invoice number. Accountants can also make a rule to flag unusual invoice amounts for review before approving them for payment. |

Dynamic discounting programs | ML is used to identify the best suppliers in business and offer customized discounts to them. |

Advanced analytics | AI is used to generate detailed system reports to gain visibility into invoice failures, noncompliance with payment terms, impact of discount programs, and other processes. |

Reason #3. Accountants are expected to take up more strategic roles

One goal of automating accounting tasks is to launch accountants into more strategic roles, such as business advisers, compliance or fraud detection experts, and AI automation leaders.

As robots take over some parts of accounting jobs, the center of accountants’ activity will shift from conducting audits and preparing reports to interpreting and analyzing data.

New age accountants need to be experts at:

Extracting relationships between data

Telling a story around it

Presenting key findings and recommendations concisely

What does this mean for you? As an accountant, you’ll have more time on your hand than before. Use it to hone your analytical skills. You can become a data scientist with accounting expertise at the core and a practical know-how of data analytics.

Analytical abilities, combined with communication skills, would enhance your storytelling prowess and help you give the decision support businesses look for in accountants.

Reason #4. Specialists required to find valuable AI use cases

AI promises to deliver insights, but its application is a struggle, and the problem compounds due to the lack of available skill sets. To sort these implementations challenges, finance leaders are working on their talent strategies in three ways:

Hiring new AI-specific talent from outside

Upskilling current finance talent in AI

Borrowing AI talent from IT departments

32% of leading AI finance firms are hiring AI-specific talent from outside compared to only 10% of other finance firms using AI in operations, according to Gartner.

What does this mean for you? AI implementation requires not only finance and accounting natives who know the core processes but also people who understand the complexities of applying AI in a business setting. Cultivate the knowledge of both AI and business processes to tailor use cases for your business’s finance needs.

A deeper working knowledge of AI applications will garner leaders’ confidence in your abilities and help overcome their reluctance to work with AI. In a nutshell, a strong foundation in both financial analytics and data can help you become a successful AI implementation leader.

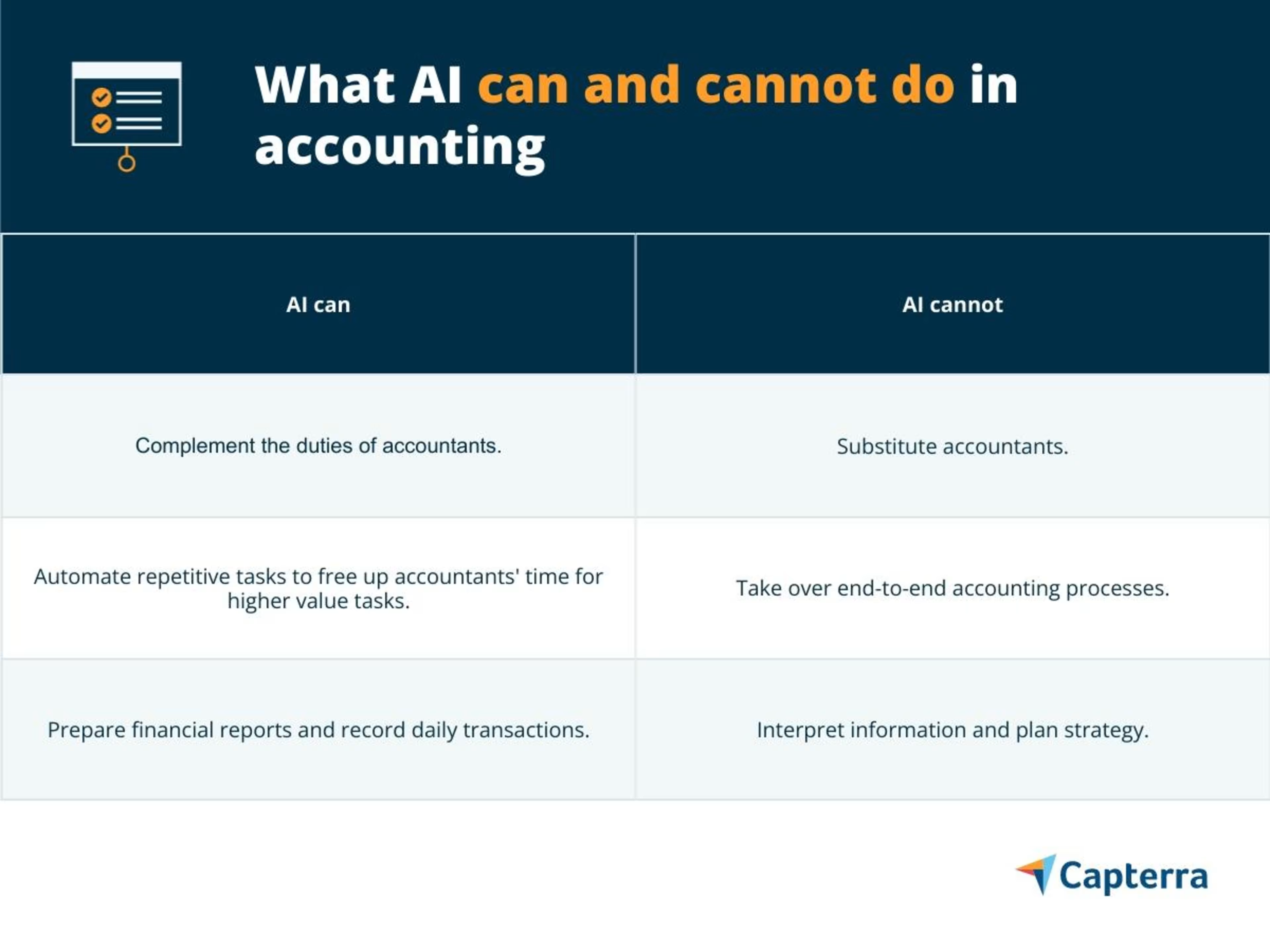

The big debate: Will AI render accountants jobless?

Even a casual discussion on automation tends to head toward the question: Which jobs will AI replace?

Robots are coming but not in the way you think.

As technology such as AI becomes widespread, some accounting tasks will be automated, but the U.S. Bureau of Labor Studies says, “This change is not expected to reduce the overall demand for accountants and auditors.” Rather it’ll make accountants more efficient by giving prominence to their advisory and analytical duties.

Robots are limited by the past data they learn from and are restricted in their functions by the parameters set by humans. Understanding the wider implications of financial data still requires human judgment.

So, the final verdict is that intelligent machines are unlikely to unseat humans in the next decade. But they’ll become a valuable tool to streamline routine activities (such as data entry and payroll management) and give human workers more space for creative problem-solving.

Next step: Start upskilling with these baseline AI skills

Gaining skills in AI and ML requires competencies in three aspects of data science:

Statistics

Programming

Business processes

Statistics is learning to collect data, describe it, and take out inferences. It’ll help you find data that answers questions such as who your top suppliers are and why.

Programming is about writing short programs to instruct a computer/software application to carry out tasks such as automating data entry and probing the data to answer specific questions. JavaScript and Python are the most commonly used languages for AI programming.

An understanding of business processes is what differentiates finance-based AI talent from IT-based AI talent. Inherent knowledge of the accounting profession, combined with statistical analysis and programming skills, makes them stand out in the AI age. Develop an analytical understanding of how everyday finance tasks are performed and how they contribute to business outcomes and objectives (e.g., more sales).

While these three competencies are a good place to start, consider joining a training program or an online course relevant for financial analysts. It’ll streamline the process of gaining new skills.

Learn more on how automation is transforming accounting processes with Capterra’sblog on “RPA in Accounting and Finance: Here’s All You Need to Know”.