Learn the pros and cons of the four major employee-benefits provider types to make the right choice for your business.

Thanks to ever-changing regulations, ever-evolving technology, and ever-heightened expectations from employees demanding experiences at work that are as seamless as the ones in their daily lives, offering benefits to your employees has never been more complicated or fraught with potential pitfalls.

That's why choosing the right employee benefits provider for your business is so important. Your provider needs to be a reliable partner that can help you deliver benefits that will attract top talent and retain your best workers, not a dicey, nondescript service that's bound to let you and your employees down.

Comparing 4 major employee benefits provider types

To help you make the best decision, let's look at four major types of employee benefits providers—insurance companies, benefits administration software vendors, professional employer organizations (PEOs), and niche benefits providers—to determine which meets your needs.

Option #1: Insurance companies

Aetna has a section of their website dedicated to employers. (Source)

Let's start at the source: insurance companies (also known as insurance carriers). As a business, you can work closely with insurance companies through their network of associated agents and brokers to offer important employee benefits like health and dental insurance.

Your most direct route to working with an insurance company is through what's called a captive agent: an agent that represents just that one insurance company. The benefit of a captive agent is that they'll know more about that insurance company's offerings and limitations than anyone. The downside? They can't recommend options from another insurance company.

Working with an independent agent—who represents multiple insurance companies—gives you more options. But be careful: Since independent agents are paid on commission by insurance companies based on the policy premium they secure from you, they may be incentivized to offer bells and whistles in your benefits offerings that you don't need.

You can also pay a broker—who works on your behalf instead of the insurance company's—to find the best employee benefits provider for your needs. Brokers tend to get less support from insurance companies than agents though, which may hinder both the benefits options they are able to offer and the information they have about them.

Recommendation: If you're looking for the best rates on your benefits offerings, you would be wise to work closely with insurance companies. But be wary of scams and unnecessary costs. If you work with multiple companies (which is likely), you'll also need to figure out a streamlined solution for benefits administration.

Option #2: Benefits administration software vendors

Benefits administration software allows your company to administer various types of benefits to your employees, track participation, generate compliance reports, and more.

Most benefits administration software vendors partner with brokers to provide benefits, but some vendors—like Zenefits—employ licensed brokers to work more closely with clients (though you should ask if they're licensed in your particular state). If you have existing benefits offerings, you'll likely be able to integrate them with your benefits administration software, but talk to vendors first to make sure.

One great thing about benefits administration software is that if it's part of a more comprehensive HR software suite (with applications for needs like recruiting, time tracking, and payroll), you'll save time through automation. For example, benefits costs are automatically deducted from employees enrolled in benefits during payroll. This also keeps all of your employee data housed in one location.

There are some potential drawbacks with this option. For one, if your software isn't intuitive, employees can get frustrated when enrolling in benefits or changing their elections, which could lead to implementation failure. You also need staff to handle benefits administration internally, which isn't always easy for smaller businesses.

Recommendation: Benefits administration software is the best solution to provide and administer employee benefits in-house if you have the staff to handle it, and are willing to do the due diligence to research and find a user-friendly system.

Option #3: Professional employer organizations (PEOs)

Selecting employee health benefits in Justworks PEO (Source)

If you don't want the burden of handling benefits administration yourself, you may want to consider contracting a professional employer organization (PEO). A PEO will act as your entire HR department for a fee, handling needs like compliance, recruiting, payroll, onboarding, time and attendance, and benefits administration.

One advantage of a PEO is that you enter a “co-employment" relationship with them, which means the PEO becomes the employer of record for your workers (the PEO appears on their paycheck and their W-2s, for example). If the PEO fails to pay necessary taxes or provide expected employee benefits, it's held liable instead of you.

This co-employment relationship also means that PEOs essentially act as one large enterprise on behalf of smaller clients. As a result, these organizations can offer more comprehensive and varied benefits options at lower rates than you would be able to get on your own.

The downside here is that PEOs are really only an option for small businesses. The typical PEO user only has around 25 employees, and after 100 employees, PEOs become cost-prohibitive compared to an internal HR department. Your employees are also at the mercy of your PEO's HR service delivery, which may be lacking compared to what you could offer in-house.

Recommendation: If you're a small business without an HR department, a PEO is a great option as an employee benefits provider. If you have more than 100 employees, or are expecting to grow to that size soon, you should look at other options.

Option #4: Niche benefits providers

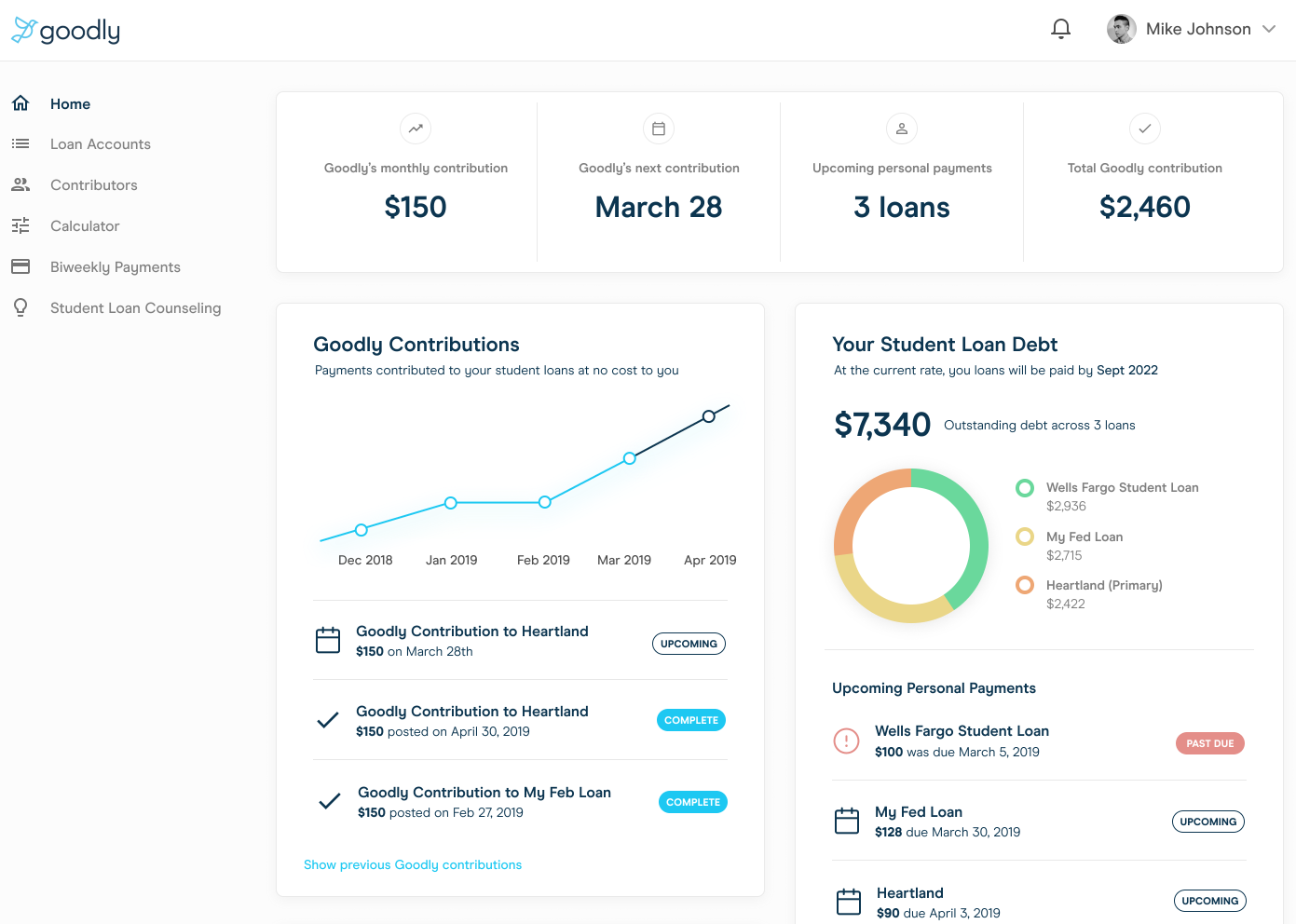

You can offer employees student loan debt repayment through Goodly. (Source)

We're using “niche benefits providers" here as a catch-all for both smaller providers of major employee benefits like health insurance and 401(k)s, and those that specialize in offering more ancillary employee benefits.

For example, many local credit unions are able to offer health insurance benefits to client businesses through partnerships with insurance companies. Options are often limited, but this could be a route to explore if you're a smaller business and already a credit union customer.

There are also companies and software vendors that specialize in providing niche employee benefits such as tuition reimbursement or pet insurance. Because these offerings aren't as popular, these niche providers may be your only option for offering these benefits. The downside here, of course, is that options are limited, and you lose economies of scale by having to contract one provider for a single benefit.

Recommendation: For some benefits, niche providers may be your only option. That doesn't negate the fact that there are often fewer options to choose from, and that contracting these providers usually comes at an extra cost.

3 tips for selecting employee benefits providers

It's easy to get overwhelmed when researching and comparing employee benefits providers. Agencies and vendors may not have your best interests in mind, and it's not as if insurers are eager to explain the differences between an HMO, an HSA, and a PPO, for example.

Throughout your search, be sure to keep these three tips in mind when talking to employee benefits providers to ensure you end up with a great benefits partner:

Compliance is key. Employment laws, especially those surrounding health insurance and 401(k)s, are forever in flux, and the last thing you want is to be flagged for noncompliance. Ask your provider about who is responsible for keeping your business compliant over time, and how you'll be notified of impactful changes.

Yes, a human touch still matters. Providers are eager to talk about how great their technology is at making things easy for employees when it comes to their benefits. That's great, but don't forget that good human customer support is vital to answering employee questions and informing benefits election decisions. Ensure providers aren't skimping in this area.

Data drives better benefits decisions. The more data you have surrounding benefits costs and elections, the better you'll be able to sculpt your employee benefits package over time to minimize costs and maximize results. Always ask providers about the data you'll have access to, and do a deep dive on any analytics capabilities that are offered.

Still have no idea what you're doing when it comes to employee benefits? Check out our four-step guide to creating an exceptional employee benefits package here.