Use this guide to learn what goes into preparing an accurate balance sheet.

As an entrepreneur or a business owner, one of the biggest mistakes you can make is not taking the time to study your company’s financial statements. And worse still, not preparing them at all.

A balance sheet is among the most notable financial statements used to monitor the financial health of your business. For management, it informs internal decision-making, and for lenders and investors, it offers a quick look into your company's capability to make profits and pay back debt.

You can prepare a balance sheet on your own or hire accountants and bookkeepers to do it for you. Another way is to hand over the responsibility to an outside specialist firm by outsourcing the job. No matter which path you take, it’s important to understand how a balance sheet works as well as the basic steps to prepare it.

This article is for anyone who wants to understand how to prepare a balance sheet, which is often used by investors, creditors, and management. We explain why and how to create one as well as suggest technology tools to simplify your job.

/ What is a balance sheet?

A balance sheet summarizes your firm’s current financial worth by showing the value of what it owns (assets) minus what it owes (liabilities). It can be understood with a simple accounting equation:

Assets = Liabilities + Shareholders’ Equity

Preparing a balance is like creating a blown-up version of the above equation by vertically dividing the sheet into two parts with assets listed on the left, and claims of owners (equity) and liabilities are on the right. The two sides must always be equal.

Why should you create a balance sheet?

The purpose of creating a balance sheet is to know the financial position of your business, particularly what it owns and what it owes by the end of an accounting period (usually after every 12 months). Therefore, a balance sheet is also called a position statement or a statement of financial position—it provides a snapshot of all assets and liabilities at a particular point in time.

Three ways using a balance sheet benefits your business:

It provides the basis for assessing risks and returns. By comparing your current assets against current liabilities, you can determine if you have enough capital to cover short-term debts (e.g., wages, lease payments) or if you need more to run everyday operations.

It’s instrumental in securing loans and investments. Most lenders and investors assess the balance sheet to see if your business can collect payments from clients, repay debts on time, and manage assets responsibly.

It shows the long-term sustainability of your business. By analyzing your balance sheet and finding out appropriate financial ratios from it, you can assess your business’s position in terms of profitability, productivity, and liquidity. You can also use these ratios to compare your performance against competitors’.

4 tasks to complete before preparing a balance sheet

To create a balance sheet, you have to follow an order and prepare a few things first—like you would have to do for many other business processes.

1. Adjust entries in the general journal

Adjusting journal entries is necessary before preparing the four basic financial statements, including the balance sheet. It means updating your accounts at the end of an accounting period for items that are not recorded in your journal.

For instance, if you delivered goods worth $5,000 on the last day of the month but didn’t receive the amount until the next accounting period, then you’ll need to adjust your journal entry. Update your accounts by making such adjusting entries in the general journal.

What is a general journal?

A general journal is the first place where daily business transactions are recorded by date. Depending upon the practice followed in an organization, some may keep specialized journals such as a sales journal, cash receipts journal, and purchase journal to record specific types of transactions.

2. Post general journal transactions to the general ledger

After transactions are recorded and adjusted for in the general journal, they are transferred to appropriate sub-ledger accounts, such as sales, purchase, accounts receivable, inventory, and cash. This process is called posting.

While a general journal records business transactions on an everyday basis, general ledgers group these transactions by their accounts. The accounts are then aggregated to a general ledger at the end of the accounting period. The general ledger acts as a collection of all accounts and is used to prepare the balance sheet and the profit and loss statement.

3. Generate the final trial balance

Once you have adjusted journal entries and posted them in the general ledger, construct a final trial balance. Trial balance is a report that lists general ledger accounts and adds up their balances. Generating the trial balance report makes it much easier to check and locate any errors in the overall accounts.

The sum of all debits must always equal the sum of all credits in a trial balance report. If it doesn’t, it means there are errors you need to track down. You may have missed a transaction or calculated something incorrectly.

Use software for bookkeeping

Accurately recording financial data is a prerequisite for effective financial reporting. Indeed, you can still do your bookkeeping with pencil and paper. But, manual bookkeeping takes much longer and leaves space for human errors.

All accounting software tools generate trial balance as a standard report. You can streamline everyday bookkeeping tasks and ensure bookkeeping accuracy using accounting software.

4. Generate the income statement

An income statement is prepared before a balance sheet to calculate net income, which is the key to completing a balance sheet. Net income is the final amount mentioned in the bottom line of the income statement, showing the profit or loss to your business. Net income is added to the retained earnings accounts (income left after paying dividends to shareholders) listed under the equity section of the balance sheet.

Prepare an income statement by taking income and expense items (such as sales) from the trial balance and organizing them in a proper format.

Now that you understand the basics, let’s discuss (in the next section) the six steps to prepare a balance sheet.

Step #1: Determine a reporting date for the balance sheet

A balance sheet determines the financial position of your business at a particular point in time, not for a period. Thus, the header of a balance sheet always reads “as on a specific date” (e.g., as on Dec. 31, 2021).

A balance sheet is usually prepared at the end of a financial year (typically every 12 months on the last day of March or December), but it can be created at any or multiple points in time, say quarterly or half-yearly.

Step #2: Collect accounts that go on the balance sheet

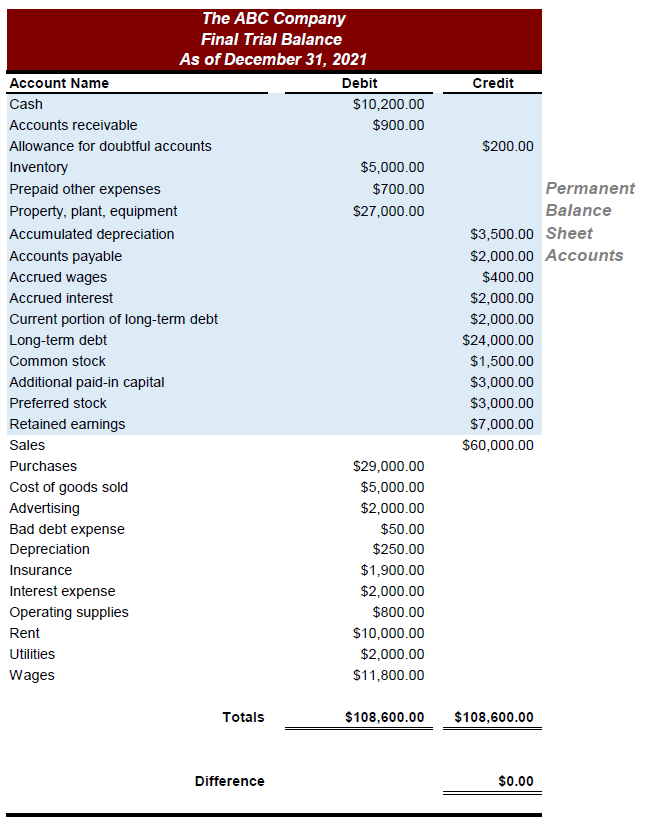

From all the accounts mentioned in the general ledger and trial balance report, the balance sheet shows only the permanent accounts ( e.g., cash, fixed assets). Permanent accounts are those accounts whose balances are carried over to the next period.

Identify these accounts and note their balances. An example of permanent accounts or balance sheet accounts on a trial balance report is given below.

Illustration of balance sheet accounts in a trial balance report

Step #3: Calculate the total assets

The next step is to identify accounts from your trial balance that represent what you own—in other words, your assets such as cash and inventory. List them on the left to create the asset side of the balance sheet. You can classify asset accounts further into two types: current and noncurrent.

Current assets include assets that can be converted into cash as early as possible (typically within the next 12 months). Current asset accounts include cash, accounts receivable, and inventory.

Cash refers to both cash in hand and at the bank.

Accounts receivable refers to transactions for which money is yet to come from your customers—i.e., the amount you are owed.

Inventory is usually the biggest portion of current assets. On the balance sheet, it includes goods that are ready for sale as well as raw materials or half-done products.

Noncurrent assets include assets that cannot be converted into cash within the next 12 months. They are used to run daily business operations. Examples are plant/factory, machinery, furniture, and patents and copyrights (intangible assets).

List the values of each current and noncurrent asset component from the trial balance account, and add up the total current assets and the total noncurrent assets to calculate the grand total of assets.

Step #4: Calculate the total liabilities

Identify accounts from your trial balance that represent what you owe—in other words, your liabilities such as accounts payable (bills that you need to pay) and loans. List them on the right to create the liability side of the balance sheet. You can classify liability accounts further into two types: current and noncurrent liabilities.

Current liabilities are obligations or debts that are payable soon, usually within the next 12 months. They are also called short-term liabilities. Accounts payable and accrued payroll taxes are some commonly used current liability accounts.

Accounts payable includes bills or transactions for which money is yet to be paid to the suppliers or creditors. This is the amount you owe to others.

Accrued payroll taxes include the part of compensation your firm owes to employees and hasn’t been paid yet for the year, such as bonuses.

Noncurrent liabilities are obligations that will take more than the next 12 months to be repaid. They are also known as long-term liabilities. Examples include employees’ pensions.

List the values of each current and noncurrent liability component from the trial balance account, and add up the total current liabilities and the total noncurrent liabilities to calculate the grand total of liabilities.

Step #5: Arrange assets and liabilities in proper order

Once you have the assets and liabilities sections ready and sorted, arrange them in proper order. Assets should be arranged in the order of liquidity and liabilities in the order of discharge ability.

Arranging assets in the order of liquidity means putting assets that can be readily converted into cash at the top of the list and more permanent assets at the bottom. Similarly, arranging liabilities in the order of discharge ability means putting short-term obligations that are payable in the immediate future first and long-term and more permanent liabilities at the bottom.

Order of liquidity for assets | Order of discharge ability for liabilities |

|---|---|

Cash in hand Cash at bank Accounts receivable Vehicles Furniture and fittings Plant and machinery Land and building | Bank overdraft Accounts payable Creditors Loans Capital |

Step #6: Calculate shareholders’ equity

Mention shareholders’ equity on the right side of the balance sheet, right below the liabilities section. Shareholders’ equity, also known as the net worth of a company, shows the value of your business if it were to be liquidated or closed down.

It includes two types of investments: capital contributed by investors/owners and the earnings or losses accumulated in the business. The most common accounts listed under shareholders’ equity are common stock, preferred stock, treasury stock, and retained earnings.

Common and preferred stocks are the shares issued by a company. Common shares give voting rights to the owners, but in the event of a company being closed, common shareholders are paid back only after preferred shareholders.

Treasury stock refers to the shares repurchased from investors to protect the firm from a hostile takeover.

Retained earnings include earnings that are reinvested in the business. It’s calculated by adding net income to previous period’s retained earnings and deducting the amount paid to investors as a share of profits.

List the values of each shareholders’ equity component from the trial balance account, and add them up to calculate total owners’ liabilities. Next, calculate the total liabilities and shareholders’ equity by adding the final sum from step 4 and step 6.

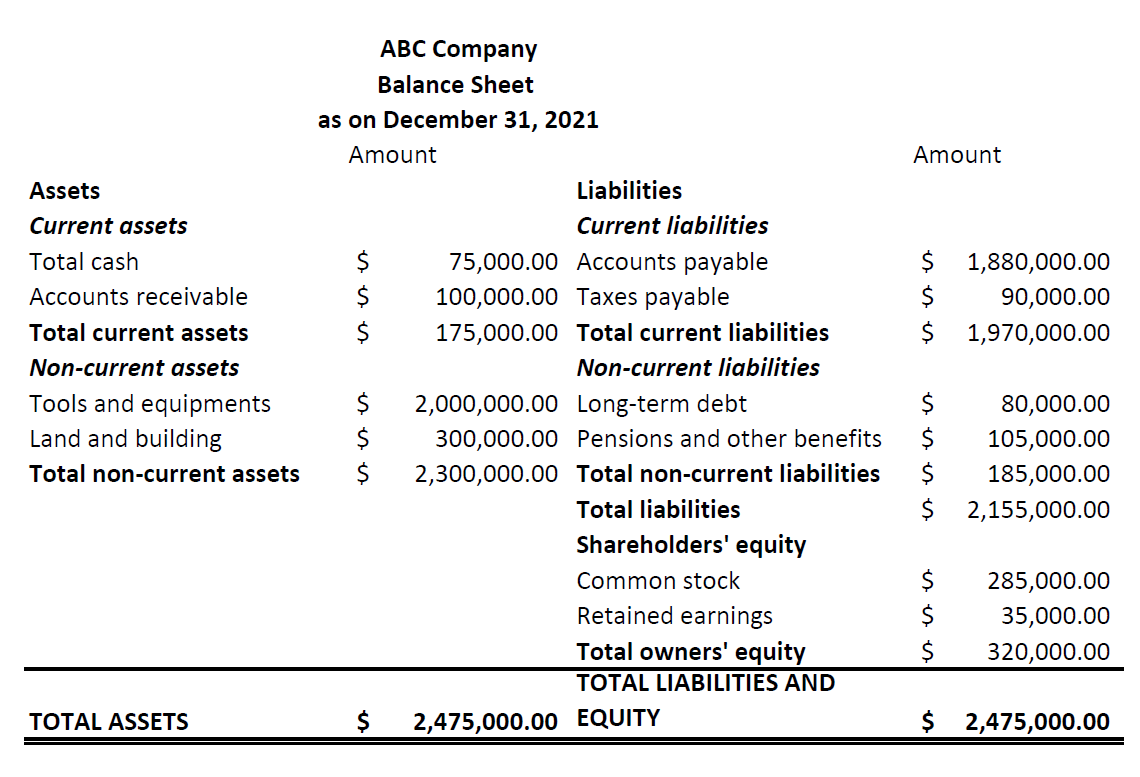

Once this is done, you’ll have a complete balance sheet ready for you. Make sure the balance on the left side matches the balance on the right. If not, check your values again.

Illustration of a balance sheet with total assets matching total liabilities and owners’ equity

Prepared the balance sheet for your business? Check out how to analyze the numbers on your balance sheet to gain actionable insights into your financial health.

Tools and tips for creating a balance sheet accurately

The integrity of a balance sheet is directly related to the information that goes into its preparation. Like most of your accounting tasks, accounting software can revamp recordkeeping and do much of the legwork while reducing errors. Use it to build a general ledger and trial balance with ease.

Doing key calculations and finding appropriate accounting ratios, such as working capital and debt-to-equity ratio, are key to analyzing your balance sheet. Financial reporting applications can help you interpret these ratios and understand the balance sheet.

Prepare a cover letter explaining the key points in the balance sheet when sending it to business leaders. Doing this will establish effective financial reporting practices that bring value to your business.

Thinking about hiring an accounting firm for help preparing your balance sheet? Browse our list of top accounting firms and learn more about their services in Capterra’s hiring guide.